MBA Guide to Higher Mortgage Interest Rates, Part 2 — How Much Money Will You Save?

--

The economics of buying a house have changed dramatically since the end of 2021. Interest rates are going up for the first time in a long time. Rates have already gone up a lot as of June 2022…and it seems likely they will continue to go up from here.

Related

• 4 Lessons on When to Sell $400,000 Worth of Stock in an Unpredictable Market

• When Is a Stock Market Crash Not Really a Stock Market Crash?

• When Is a Bear Market Not Really a Bear Market?

Recent

• The Deafening Silence on Stock Buybacks from Centrist Democrats

• 2 Reasons Populations Are Collapsing in Developed Countries

• 3 Key Facts Everyone Is Missing About Biden’s Student Loan Debt Relief

Potential to Change the Way You Think

• Why Are Fundamental Human Values Critically Important for Successful, Enduring Brands?

• Life Expectancy vs. Healthcare Costs in the U.S. (and Japan, Germany, France, Spain, Portugal, etc.)

• (1a/9) “Top-Down” Makes More Sense Than “Left-Right” in the U.S.

This is Part 2 of a series articles on ways of dealing with these high(er) interest rates as best as you can and decreasing the amount of mortgage interest you pay.

In this 2nd article, I’m going to:

- Do a quick recap of the takeaways from Article #1 (Part 1 of the MBA Guide to Dealing with Higher Mortgage Interest Rates)

- Explain why paying “extra” each month on your mortgage can make such a big difference in the total amount of interest you pay over the lifetime of your mortgage.

- Explain how much of a difference these extra payments can make.

- Look at examples of these “extra payments” in action.

- Leave you with 5 main takeaways.

Caveats:

- I am not a licensed financial advisor. Do your own homework after reading this (but if you have questions I can answer or help guide you with, please post them in the comments section below.)

- I am not invested one way or the other in residential or commercial real estate or any housing/real estate stocks or other investment vehicles. It doesn’t matter to me if you buy a house or not — I do not benefit financially either way. My only goal is to help you make the smartest decision(s) you can so that you keep as much of your money as possible in your own pocket.

Section 1. Quick recap of the takeaways from Part 1 of the MBA Guide to Dealing with Higher Mortgage Interest Rates

- Buying a home is the largest purchase that most people make in their lives. Getting it right — or, as right as possible — is incredibly important to regular working Americans.

- Unfortunately, the advice they get on how to take the best possible care of themselves financially on this “biggest purchase of a lifetime” often comes from pundits, authors, and/or financial services industry people who have interests that run counter to yours.

- Interest rates have broken through a very long-term downward trendline. Rates have already moved upwards quite a bit, and it seems as though there will be further increases in mortgage interest rates over at least the next year.

- Few financial pundits on TV or authors or financial advisors focus on the “total amount of mortgage interest you will pay” as something homebuyers should be concerned about.

- As interest rates increase, the “total amount of mortgage interest” you will end up paying over the lifetime of your mortgage goes up dramatically.

Section 2: Why paying “extra” each month on your mortgage makes such a big difference in the total amount of interest you pay over the lifetime of your mortgage

Currently, 30-year fixed-rate mortgages are running at just under 6.00% interest.

Imagine that you are buying a $500,000 house and you are putting 20% — $100,000 — down as your downpayment. That means your mortgage is going to be for $400,000.

Over the course of a fixed-rate 30-year $400,000 mortgage at 6%, you would pay a total of $463,353 in interest alone.

In other words, at 6%, you will pay more in interest than the house itself actually cost. Your TOTAL payments — including both principal of $400K and $463K in interest — would be $863,353.

And that’s at 6%. If interest rates continue to rise to 7% or 8% or 9%, the total interest amounts increase dramatically.

Section 3. How much of a difference these extra payments can make

Pay extra each month with your mortgage payment.

That’s it.

(…although as we get deeper into the next couple articles, I’ll share some different ways of approaching and thinking about this that I think will have you looking at paying off a mortgage differently as you go forward.)

There are a few different ways of conceptualizing how you pay extra each month. For now, I’m going to keep things simple.

We’re going to assume that you will pay X percent of your normal monthly mortgage payment as your “extra” each month. Same amount extra each month — the models below will assume you don’t change the extra amounts from month to month.

So if your normal monthly mortgage payment would be $2500, then 1% of that is $25.

- 2% would be $50.

- 3% is $75.

- 4% is $100

- 6% is $150. And so on.

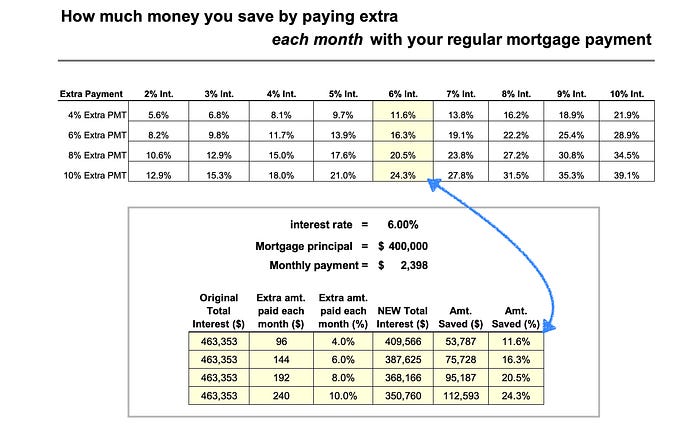

In our examples below, I’m going to use 4%, 6%, 8%, and 10% as four different levels of payment you could choose to go with.

Most of the numbers I’ll use will assume a mortgage interest rate of 6.00%. But you’ll see in the table above that show what percent of the “original total interest amount over 30 years” you would save at different interest rates — not just at 6%.

For instance, at 6% interest, if you pay an extra 10% each month on your mortgage, you will save over 24% of the interest you would otherwise have paid — that’s over $112,500! So instead of the original $463,300, you would instead “only” pay $350,800. (I’m rounding off the numbers just a bit in this paragraph; exact numbers are in the tables above.)

The amount you choose to go with is entirely up to you. Whether it’s 4% or 7% or 12%, I recommend basing it on how much “extra” money you have and how much you value decreasing the amount of interest money you’ll pay over the 30 year term of your mortgage.

Section 4. The mechanics of how total interest can decrease so much by making what *seem* like relatively small additional monthly payments.

- When you start out in the very first month of your 6%, 30-year fixed-rate $400,000 mortgage, your first monthly payment will be $2398.

- Of that $2398, (1) the amount going to pay interest will be $2000, and (2) the remainder — $398 — will go toward the principal.

- That means there is still a huge amount of principal left going in to Month 2 of the mortgage — $399,602 — that will accrue interest. For Month 2, the interest portion of your $2398 payment will be $1998, leaving an even $400 to pay down a bit more of the principal. At the end of Month 2, your remaining principal will be $399,202.

- At this point, you can probably see very clearly why — at this pace — it’s going to take 30 years (or 360 months) pay off your $400,000 mortgage!

- Now let’s jump ahead almost 30 years…!

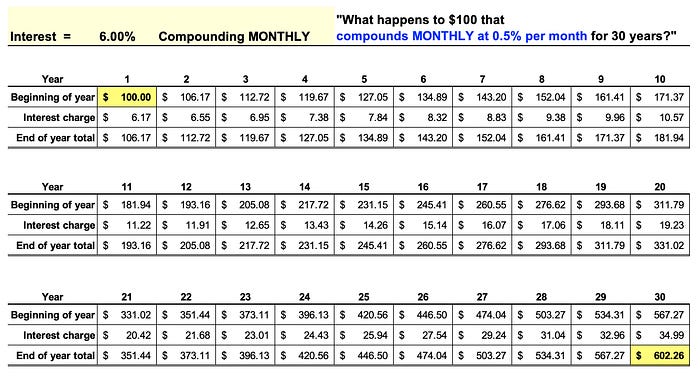

- Think about the very last $100 that you’ll pay on your mortgage in the 12th month of the 30th year. (See the table above this list for what it looks like when $100 compounds ANNUALLY at 6% per year.)

- That $100 is going to have been getting charged interest in EVERY SINGLE MONTH over the previous 29 years and 11 months. And the interest from the first month also has additional interest building up on it, same as the interest charge from the second month and the third month and the fourth month…..you get the idea.

- Now, 6% interest per year might not sound like that much, but when you compound it monthly over 30 years…? Yep, it gets a LOT bigger.

- How much bigger?

- When you compound the interest ANNUALLY over 30 years (6% interest per year), it works out to about $474 in interest on top of the original $100 in principal that still has to get repaid in the very last month of the mortgage. So in Year 30, paying back that original $100 will cost you a total of $574.35.

- When you compound the interest MONTHLY over 30 years (6% interest per year is 0.5% interest per month), it works out to about $502 in interest on top of the original $100 in principal that still has to get repaid in the very last month of the mortgage. (See the table below for details on when interest on $100 compounds MONTHLY over 30 years.)

- Did you catch that? If you pay an extra $100 in the very first month of your mortgage, that means the total amount of interest you will pay over the lifetime of your mortgage will decrease by $502. So in Month 12 of Year 30, paying back that original $100 will cost you a total of $602.26.

Ok, now let’s imagine that — in addition to your $2398 per month mortgage payment — you also pay an additional $96 per month. So your total MONTHLY payment is going to be $2494. That extra $96 works out to be about 4.0% extra each month.

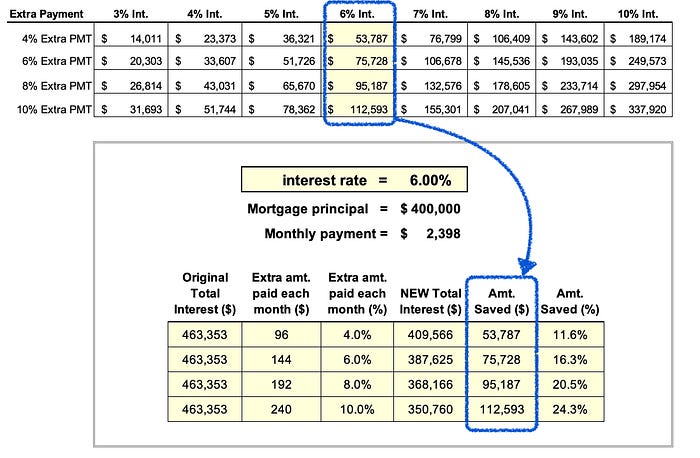

Paying the extra $96 per month until your mortgage is paid off will save you almost $54,000 — or $53,787 to be exact. See the first line in the blue circles immediately below.

As you look at the clustered bar groups in the chart below, I would recommend:

- Just look at the 6%, 8%, and 10% groupings — the ones that have the blue circles drawn around them.

- Then compare the same color of bar from all three bar groups. For instance, look at how the 4% extra payment (the blue bar on the left of each cluster) saves almost $54,000 when mortgage rates are 6%, but it jumps all the way up to $189,000 that you save when interest rates are 10% and you pay only an extra $96 per month!

If you have any questions as you are going through this, please post them in the replies section at the bottom, and I’ll be happy to answer them.

It’s worth spending a couple minutes looking at the different amounts you can save (1) at different mortgage interest rates (listed above for 3% to 10%) and (2) based on different “extra amounts” you choose to pay each month (listed above for 4%, 6%, 8%, and 10%.)

Section 5. Short list of takeaways

- You will save large amounts of money if you pay extra on your mortgage each month. If you don’t take anything else away from this article, remember this point.

- If you keep constant the “extra amount” you pay each month — i.e., for a moment, just look at the 10% extra payments (the purple bars on the right end of each cluster of bars) — you can see that the amount of money you save starts to increase a LOT as mortgage interest rates go up. In other words, “paying extra each month” is your good friend when interest rates are high…and becomes an even better friend as interest rates keep going up.

- At 6%, mortgage rates today are already high enough to make it worthwhile paying extra for most people.

- For this article, I modeled the extra monthly payments as being “the same amount extra” each month to keep things simple. However, there is no reason why it has to be the same amount extra each month. If you have extra money coming in this month and you want to increase that extra amount, go for it. Do it. Don’t hesitate, especially if you’re still early in the 30-year term of the mortgage.

- Extra payment in the early years of your mortgage save you more money — potentially a lot more — than the same amount of “extra payment” toward the end of your mortgage term. I’ll talk about this more in the next couple articles.

We still have more ground to cover in the next few articles. (Yes, this is going to go longer than the original “3 parts” I envisioned.)

Part 3 — the next article — will touch on another big benefit of paying extra each month. This “big benefit” really is a big deal, and it has some interesting implications for your financial planning.

Again, if you have any questions or comments about the material we have covered so far, please share them in the comments/replies section below.

Related

• 4 Lessons on When to Sell $400,000 Worth of Stock in an Unpredictable Market

• When Is a Stock Market Crash Not Really a Stock Market Crash?

• When Is a Bear Market Not Really a Bear Market?

Recent

• The Deafening Silence on Stock Buybacks from Centrist Democrats

• 2 Reasons Populations Are Collapsing in Developed Countries

• 3 Key Facts Everyone Is Missing About Biden’s Student Loan Debt Relief

Potential to Change the Way You Think

• Why Are Fundamental Human Values Critically Important for Successful, Enduring Brands?

• Life Expectancy vs. Healthcare Costs in the U.S. (and Japan, Germany, France, Spain, Portugal, etc.)

• (1a/9) “Top-Down” Makes More Sense Than “Left-Right” in the U.S.

Want me to cover a topic? Please post suggestions in the comments, and I’ll use your input to help prioritize my writing and research.

If you appreciate my writing, please share it on social media.

Want unlimited access to all Medium articles? Become a member!

As always, thank you for reading, subscribing, clapping, and sharing — I appreciate you sharing your time and attention!